IRMAA - Income Related Monthly Adjustment Amounts

What is IRMAA?

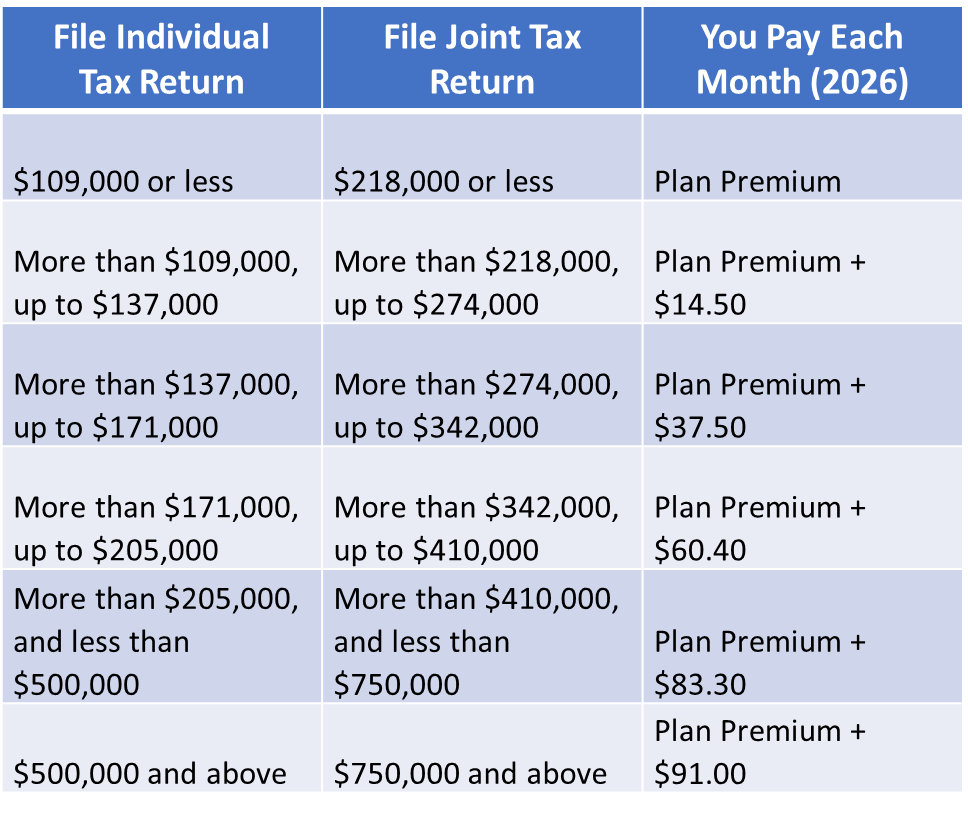

IRMAA stands for Income Related Monthly Adjustment Amounts. High-income households pay an extra charge—IRMAA—on top of the standard Medicare premium. IRMAA can apply to either Medicare Part B or Medicare Part D premiums. If you fall into one of the high-income categories—more than $109,000 for individuals and $218,000 for couples—the Social Security Administration (SSA) will notify you. The IRMAA notification from SSA might happen when you first apply for Medicare, but it can be triggered at any other time post initial Medicare enrollment if your income exceeds the threshold.

There is a two-year lookback for IRMAA. For example, if your income as reported on your tax return from 2024 fell into the high-income category, you would pay IRMAA for 2026 Medicare monthly premiums.

2026 Medicare Part B Premium & IRMAA

2026 Medicare Part D IRMAA

How to Reduce or Eliminate IRMAA if Your Income Is Lower Today Compared to Two Years Ago

Since IRMAA is calculated on your income from two years ago, many federal retirees might have less income today than when IRMAA was initially calculated. If you experience a life-changing event that reduces your income, you can request an IRMAA reduction from the SSA. Learn more here or by calling 800-772-1213.

The following life-changing events are allowed for IRMAA reductions:

- Marriage

- Divorce/Annulment

- Death of Your Spouse

- Work Reduction

- Loss of Income-Producing Property

- Loss of Pension Income

- Employer Settlement Payment

- Work Stoppage/Retirement

Most federal employees will have lower income once they retire compared to when they were active employees. Work stoppage is an allowed life-changing event, and every new federal retiree that qualifies for IRMAA should request a reduction from the SSA if they will have lower income in retirement.