Healthcare Affordability Series Part 5: Why HDHPs With HSAs Are the Most Affordable Health Plan for Most Federal Employees

Healthcare costs have climbed steadily for years with no relief in sight. For federal employees, the financial pressure is even sharper in retirement: FEHB premiums can no longer be paid pre-tax, Medicare adds new costs, and healthcare usage tends to increase with age. A recent report estimates that men will need $212,000 and women $252,000 saved just to have a 90% chance of covering healthcare expenses in retirement.

The good news? There's a savings vehicle specifically designed to help you prepare, one that works for healthcare costs today, in the years ahead, and well into retirement. It's a High-Deductible Health Plan (HDHP) paired with a Health Savings Account (HSA), and for most federal employees, it's likely the most affordable health plan available. Here's everything you need to know.

What are HDHPs?

As the name suggests, HDHPs have a higher deductible than most other FEHB plans. Until you meet that deductible, you pay the full allowed charge for covered services. Once you meet it, you usually pay coinsurance, or a percentage of the cost rather than a flat copay. Like all FEHB plans, preventive care is covered at no cost regardless of whether you’ve met the deductible.

The Built-in HSA

What sets HDHPs apart is that enrollment automatically comes with an HSA, and the plan contributes money to it on your behalf. These contributions, known as premium pass-throughs, are deposited monthly. For example, the MHBP HDHP contributes $1,200 annually for self-only enrollment, which works out to $100 deposited into your HSA each month. You can also make your own voluntary contributions on top of that, which we'll cover in the next section.

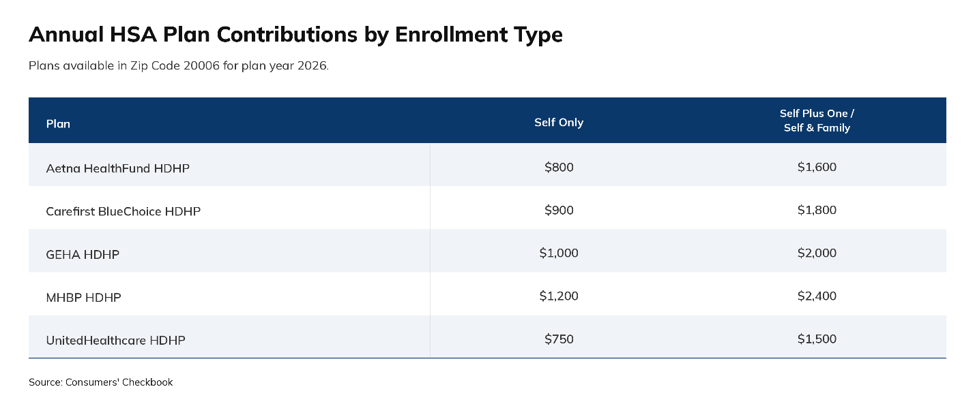

Plan options in the Washington, D.C. area

Federal employees in the Washington, D.C., area currently have five HDHP options to choose from. Annual plan contributions to the HSA range from $750 to $1,200 for self-only enrollment, and from $1,500 to $2,400 for self-plus-one or self-and-family enrollment.

How do HSAs work?

HSAs are the only savings account in the U.S. with a triple-tax advantage:

- Contributions are tax-free. Money goes in pre-tax, either through payroll deductions that reduce your taxable income, or as a tax deduction if you make a lump sum contribution.

- Growth is tax-free. Any investment gains accumulate without being taxed.

- Withdrawals are tax-free. As long as funds are used for qualified healthcare expenses, you owe nothing at withdrawal.

FEHB plans offering an HDHP partner with a financial services company to manage the HSA. Each provider typically has a range of investment options like what you'd find in an IRA so you can invest conservatively or aggressively depending on your risk tolerance.

Contribution limits

HSA contribution limits are adjusted annually. For 2026, the combined limit for voluntary and plan contributions is $4,400 for self-only enrollment and $8,750 for self-plus-one or self-and-family. If you're 55 or older, you can contribute an additional $1,000 per year as a catch-up contribution.

No "use it or lose it" rule

Unlike a Flexible Spending Account (FSA), HSA funds never expire. Your balance carries over year after year, and it can be invested to grow over time or kept in cash to use whenever you have a qualified healthcare expense.

Non-medical withdrawals

You can withdraw HSA funds for non-medical expenses, but the tax treatment depends on your age. Before 65, you'll owe a 20% penalty plus regular income tax on those withdrawals. At 65 and beyond, the penalty disappears and withdrawals are taxed like ordinary income, like a traditional IRA.

Portability

You own your HSA, so if you switch to a non-HDHP during a future Open Season, your existing balance stays yours and remains available to spend or invest. The only restriction is that you can no longer make new contributions while enrolled in a non-HDHP plan.

How to maximize your HSA

Pair your HSA with a Limited Expense FSA (LEXHCFSA): IRS rules prevent you from enrolling in a general-purpose healthcare FSA while covered by an HDHP with an HSA. However, you can pair your HSA with a LEXHCFSA. These accounts cover dental and vision expenses only, but they carry the same tax advantages as a regular FSA. Using a LEXHCFSA for dental and vision costs means your HSA funds stay invested rather than being spent on routine expenses.

Redirect any premium savings into your HSA: Depending on your current plan, and which HDHP you choose, switching plans could lower your premium. Rather than keeping those savings as a small pay bump, consider depositing them into your HSA. Since you've already been budgeting for the higher premium, you won't feel the difference in your paycheck. As a bonus, spending your voluntary contributions first keeps your plan's monthly contributions invested.

You don’t need rush to spend your HSA since the reimbursement window never closes; as long as the expense occurred after your HSA was established, there is no deadline to seek reimbursement for a qualified healthcare expense. That means you can pay out-of-pocket today, let your HSA balance grow for years, and reimburse yourself later, tax-free. Just be sure to keep your receipts and documentation in case of an IRS audit.

How much can I save with an HDHP?

Checkbook’s Guide to Health Plans models all FEHB plans on estimated yearly costs, the combination of premium plus likely out-of-pocket costs based on the characteristics of the user. Depending on your current plan, you could save thousands of dollars by switching to an HDHP.

But wait, there’s more…

When Checkbook models plans, it doesn’t know if or how much someone will voluntarily contribute to an HSA so it can’t count those tax savings into the yearly cost estimates. There are two different types you receive from voluntary contributions into the HSA:

Income tax savings. Every dollar you contribute to your HSA reduces your taxable income, lowering your federal and, in most cases, state income tax bill.

Payroll tax savings. If you contribute through payroll deductions, those contributions also avoid Social Security and Medicare taxes, a savings of 7.65%.

Factor those in, and HDHPs become an even stronger choice for those making voluntary contributions.

Do HDHPs have drawbacks?

Yes, and it's worth understanding them before enrolling.

The biggest challenge is cost unpredictability. Depending on what care you need and when, your out-of-pocket costs can vary significantly.

That "when" matters more than most people realize. If you're hospitalized late in the plan year, you've likely received your full HSA contributions and already paid down some or all your deductible, meaning your HSA funds are available to cover whatever remains. But if the same hospitalization happens in January at the beginning of the plan year, you could face the entire deductible plus coinsurance with little or no HSA balance to offset it. By contrast, many non-HDHPs charge a flat copay for hospitalizations with little to no deductible, making costs more predictable regardless of timing.

There's also investment risk to consider. If you choose to invest your HSA funds, which is one of the account's biggest long-term advantages, those investments can lose value. Depending on your fund choices and market conditions, your HSA balance could be lower than expected when you need it.

In Summary

HDHPs paired with an HSA offer federal employees something no other FEHB plan can match: a tax-advantaged way to pay for healthcare expenses today while building a financial cushion for the rising costs of healthcare in retirement. Lower premiums, plan contributions to your HSA, and tax savings from voluntary contributions can add up to thousands of dollars in annual savings, often beating popular PPO plans even after accounting for the higher deductible.

That said, HDHPs aren't the right fit for everyone. Higher out-of-pocket cost risks, the lack of transparency about what something costs both before and after the deductible, and the possibility of investment loss are real considerations, particularly for those who expect significant healthcare needs in the coming year or have limited cash reserves to cover a large, unexpected bill.

The bottom line: If you're a federal employee who hasn't seriously evaluated an HDHP, it's worth running the numbers. For most people, the savings are substantial, and the long-term benefits of saving now for retirement healthcare costs are hard to match.